Within the Year effect (WTY or Max-Min)

Within the Year effect spots for anomalies in a period inside a calendar year.

There can be a positive period of a year that goes beyond a period of a single month. Every financial instrument can have a different timespan in which its returns are significantly positive or negative. For example:

- Copper use to be strong from mid-January to mid-March, while

- EurGbp use to be weak from mid-March to the end of April.

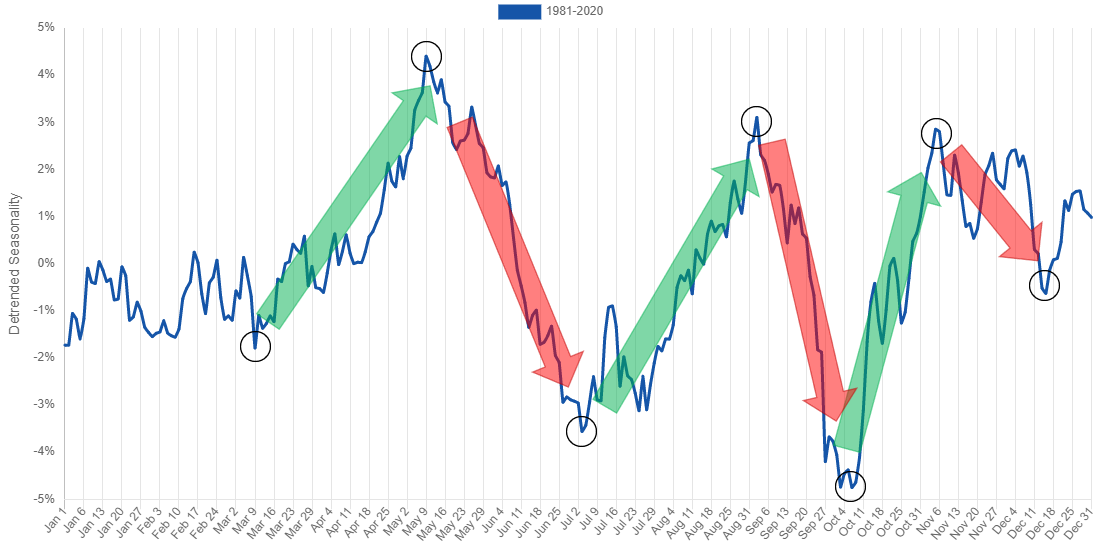

Seasonality 'Max Min' strategy

In ForecastCycles we analyze this anomaly through the "Seasonality Max Min" strategy. The strategy is built by taking the most important Maximum and Minimum from the Seasonality, computed over the entire history of the financial instrument.

The Seasonality used is the Detrended, since it is better for identifying top and bottoms.

In the Chart below, the Detrended-Seasonality of Apple, and the Max and Min identified by our algorithm:

- each green arrow identifies a long strategy

- each red arrow identifies a short strategy

In this case the indications are:

- Long: from 09.Mar to 09.May

- Short: from 09.May to 03.Jul

- Long: from 03.Jul to 03.Sep

- Short: from 03.Sep to 03.Oct

- Long: from 03.Jul to 05.Nov

At the beginning of every new-Year the Max-Min indications are updated for each Ticker, since they are computed using the entire history, and the year just closed enters in the computations.